Explain in Detail: How Private Equity and Hedge Funds Are Taxed?

Triston Martin

Feb 01, 2024

Introduction

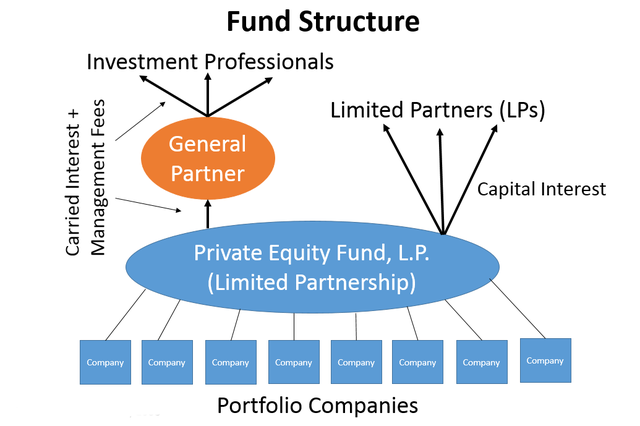

How private equity and hedge funds are taxed? It is common practice for private equity firms to pool their investors' cash and then use that money to buy and manage successful businesses. They hope to sell the companies later for a substantial profit, and until then, they want to maximise the value of the companies they own. A private equity firm's limited partners are the investors who own a portion of the firm, and the general partner is responsible for managing the firm.

Hedge funds, like mutual funds, are pools of money from multiple investors that are then invested in various securities with the hope of yielding a profit. The SEC distinguishes between hedge funds and mutual funds by noting that the former is not as subject to disclosure requirements regarding their holdings. Mutual funds are a common way to put money to work. Similar to the private equity model, the general partner of a hedge fund manages the fund, and the investors are called limited partners. The goal of hedge funds and private equity is to find wealthy people and huge organisations with the financial wherewithal to take on more risky investments. Generally speaking, the legislation specifies that an investor must be an "accredited investor" to invest in them.

In What Ways Are Private Equity And Hedge Funds Taxed?

The structure of private equity and hedge funds makes them ideal candidates for flow-through status because they function similarly to partnerships (also known as pass-through entities). By placing the onus of tax payments on shareholders, they can avoid paying taxes twice (as corporations are). Annually, the fund will issue a Schedule K-1 to limited partners. Each investor receives a detailed breakdown of their share of the fund's gains and losses to prepare their tax returns.

For this reason, limited partners do not have to pay self-employment tax for Medicare and Social Security. However, some pass-through entities, such as sole proprietorships, are subject to this tax on their taxable income. Assuming a tax rate of 15.3 percent, this exemption will prevent the first $147,000 of your income from taxing in 2022, saving you a maximum of $22,491 in that year. Different from limited partners, general partners receive further tax treatment. They typically charge 2% of assets under management annually and receive 20% of profits over the target. For tax purposes, the additional 20% is not salary but carried interest, which is taxed at a lower rate than ordinary income.

The top marginal tax rate that can be applied to regular income is 37%, but the maximum marginal tax rate that can be used for long-term capital gains is only 20%. The Tax Cuts and Jobs Act of 2017 changed the capital gains taxes, requiring investors to hold onto their investments for at least three years before they may benefit from the lower rates. In addition, carried interest is not subject to taxes that apply to earnings because it is considered self-employment income. But for most people, that 2% management charge is just another form of ordinary income. Some general partners can avoid this restriction by forgoing the management fee. Renouncing their expense in exchange for a larger share of the partnership's profits allows them to shift their income to a capital gain and pay tax on it at a more favourable rate. They can turn their regular salary into a capital gain by doing this.

Anyone Can Put Money Into Private Equity Or Hedge Fund

Private equity and hedge fund investments are only open to those who meet the "accredited investor" criteria under federal securities laws. The U.S. Securities and Exchange Commission (SEC) requires at least one of the following: Over $200,000 in average annual income over the past two years, or $300,000 with a partner or spousal equivalent, a prediction for this year is on par with the past two years. Your net worth, not counting your primary house, is over $1 million, alone or jointly. You hold a current and active Series 7, 65, or 82 licence to trade securities. A wide range of minimum investments is required to participate in various funds, from $100,000 to $550,000 to $1,000,000+.

Conclusion

Current U.S. legislation provides numerous breaks for private equity and hedge firms, resulting in lower effective tax rates. Despite widespread disapproval, these statutes continue to be in effect. Most of a fund manager's compensation comes from carried interest, taxed at lower capital gains rates than salary or wages and is therefore preferred by the manager. Although efforts to end the widespread belief that these policies only benefit the wealthy have met with failure thus far, critics continue to voice their displeasure.